Publication

Fiscal Crises (with Kerstin Gerling, Paulo Medas, Tigran Poghosyan, and Juan Farah-Yacoub) [Paper in Press] [Slides] [Data]

Journal of International Money and Finance November 2018, pp 191-207.

Mentioned in "IMF Key Issues", "April 2018 IMF Fiscal Monitor" and "UK Parliament Fiscal Risk Report"

A key objective of fiscal policy is to maintain the sustainability of public finances and avoid crises. Remarkably, there is very limited analysis on fiscal crises. This paper presents a new database of fiscal crises covering different country groups, including low-income developing countries (LIDCs) that have been mostly ignored in the past. Countries faced on average two crises since 1970, with the highest frequency in LIDCs and lowest in advanced economies. The data sheds some light on policies and economic dynamics around crises. LIDCs, which are usually seen as more vulnerable to shocks, appear to suffer the least in crisis periods. Surprisingly, advanced economies face greater turbulence (growth declines sharply in the first two years of the crisis), with half of them experiencing economic contractions. Fiscal policy is usually pro-cyclical as countries curtail expenditure growth when economic activity weakens. We also find that the decline in economic growth is magnified if accompanied by a financial crisis.

Journal of International Money and Finance November 2018, pp 191-207.

Mentioned in "IMF Key Issues", "April 2018 IMF Fiscal Monitor" and "UK Parliament Fiscal Risk Report"

A key objective of fiscal policy is to maintain the sustainability of public finances and avoid crises. Remarkably, there is very limited analysis on fiscal crises. This paper presents a new database of fiscal crises covering different country groups, including low-income developing countries (LIDCs) that have been mostly ignored in the past. Countries faced on average two crises since 1970, with the highest frequency in LIDCs and lowest in advanced economies. The data sheds some light on policies and economic dynamics around crises. LIDCs, which are usually seen as more vulnerable to shocks, appear to suffer the least in crisis periods. Surprisingly, advanced economies face greater turbulence (growth declines sharply in the first two years of the crisis), with half of them experiencing economic contractions. Fiscal policy is usually pro-cyclical as countries curtail expenditure growth when economic activity weakens. We also find that the decline in economic growth is magnified if accompanied by a financial crisis.

Working Papers

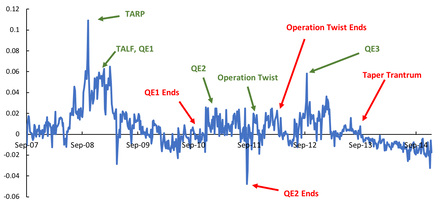

Market Expectations of Shadow Bank Systemic Bailouts Implied by OTM Put Option Basket-Index Spreads

Market Expectations of Shadow Bank Systemic Bailouts Implied by OTM Put Option Basket-Index Spreads

Shadow Banking and Systemic Bailouts [Under Revision]

We study the impact of systemic bailout expectations on bank credit growth patterns. Using daily put options data of U.S. bank holding companies, we measure each bank holding company's exposure to the systemic bailout factor, which is the sensitivity of each bank's out-of-the-money put option price to the variations of sector-wide put option basket-index spreads. We show that low market expectations of the banking sector systemic bailouts played a significant role in the weak bank credit recovery after the subprime crisis. Bank holding companies with higher pre-crisis exposure to the systemic bailout factor experienced larger post-crisis deviations from the pre-crisis bank credit growth trend. Perhaps surprisingly, such pattern is persistent even for banks that are less affected by the post-crisis financial regulations and less exposed to borrowers from the deteriorating sectors. Furthermore, we drill down to the commercial bank subsidiary level data while controlling for parent bank holding company fixed effects. This analysis reveals that commercial bank subsidiaries within the same bank holding company present same credit growth patterns even though they have different exposure to financial regulations and deteriorating sectors. To rationalize the empirical findings, we propose a model with both commercial banks and shadow banks. The securitization market, which connects the two types of banks, determines how market expectations of systemic bailouts to shadow banks affect the credit origination capacity of the whole banking system.

Non-Performing Loans, Government Interventions, and Economic Recoveries (with Aaron Tornell)

This paper studies the effects of government interventions towards bank non-performing loans (NPLs) during the aftermath of banking crises. Following the narrative approach, we constructed a cross-country database of government intervention plans for reducing NPLs. The database documented 72 systemic banking crises since 1990 and most of which are followed by direct capital injections or NPLs purchases that are conducted by the government. we expanded the existing banking crises database by providing detailed amount of direct capital injections and NPLs purchases based on IMF country reports and each country’s central bank reports. Cross-country regression analyses show that both plans contribute to higher long-run growth in credit and output. Fiscal outlays on either capital injections or NPLs purchases with 1% of crisis year GDP are followed by an additional 0.5% annual credit growth and an additional 0.12% annual output growth. In addition, direct capital injections lead to faster recoveries in credit and output in emerging market countries, while NPLs purchases with lower haircut lead to faster growth in advanced market countries. However, these intervention plans are costly, as they significantly increase the public debt. Fiscal outlays with 1% of crisis year GDP are followed by an additional 0.3% increase in the public debt ratio in the short-run, and such effect is stronger if the haircut in NPLs purchases is higher. Despite the short-run fiscal cost, we do not observe significant long-run fiscal impact after both intervention plans, which implies that government bailouts to the distressed banking sector barely cause long-term fiscal burdens.

Work-in-progress

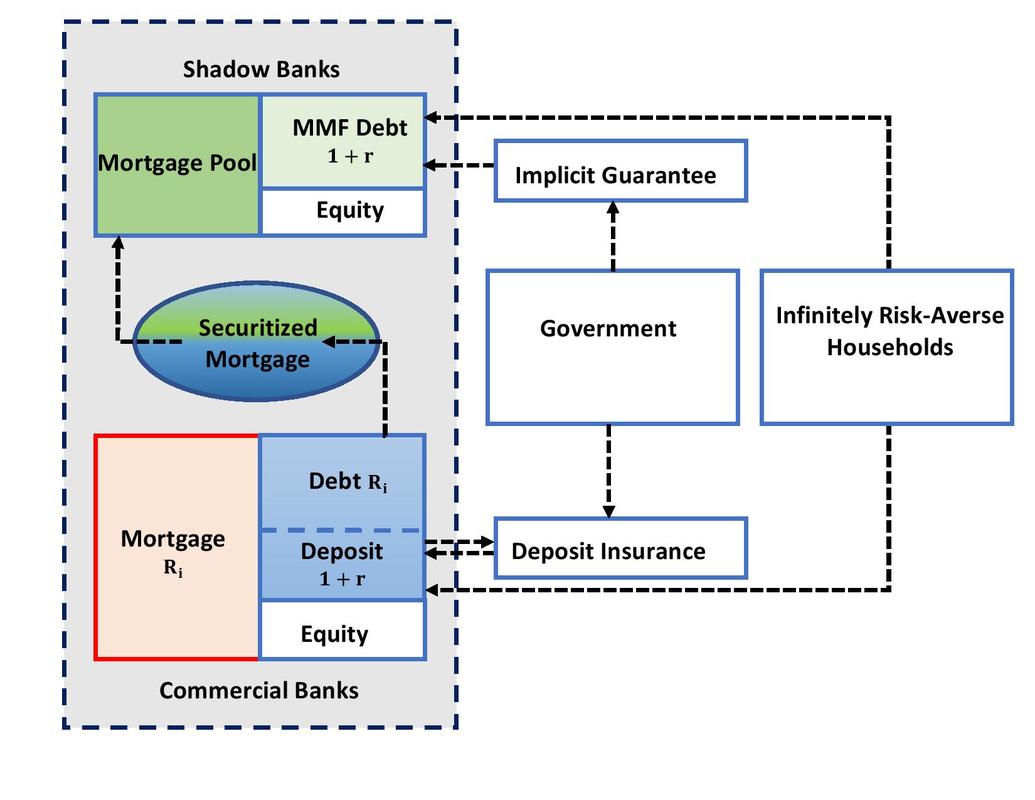

A Simple Structure of the Modern Banking System

A Simple Structure of the Modern Banking System

Shadow Bank Bailouts and Asset Flows within Bank Holding Companies: A Tale of Two Bankers [Slides]

As the government bailout guarantee to the shadow banking sector drops, shadow bankers are motivated to convert themselves to commercial bankers who are in a different safety net but subject to stricter regulations. Indeed, the bankruptcy of Lehman Brothers without government bailout was followed by a wave of conversions from shadow banks to commercial banks (including Goldman Sachs and Morgan Stanley). This paper provides a model framework to analyze the efficiency and stability of the banking sector following endogenous conversions between commercial banks and shadow banks caused by exogenous changes in the government guarantee policy. Securitization, which allows commercial banks to transfer a fraction of their balance sheet risks to shadow banks, is the key connection between these two banking sectors. The equilibrium securitization volume is determined by 1) commercial bankers’ trade-off between balance sheet risks and private benefit from deposit insurance, 2) shadow bankers’ ability to diversify their assets pool for sustaining higher leverage, and 3) the return on equity (ROE) between the two sectors. In a numerical experiment with a large drop in government guarantee to shadow banks, commercial banks expand, shadow banks shrink, and the banking sector is more stable under rational expectations. However, ROE in the whole banking sector is likely to decline and the exposure to the neglected tail risks increases as the shrinking shadow banking sector increases assets diversification to meet higher securitization requests from the expanding commercial banking sector.

Sources of Credit (with Dulani Seneviratne, Jerome Vandenbussche, and Peichu Xie)

We study if the heterogeneity in bank fundamentals contains information about future credit-related macrofinancial stability risks. We present our analyses based on (i) country-level measure of "riskiness of bank credit originations" and (ii) bank- and syndicated loan-level evidence of bank risk-taking patterns.

As the government bailout guarantee to the shadow banking sector drops, shadow bankers are motivated to convert themselves to commercial bankers who are in a different safety net but subject to stricter regulations. Indeed, the bankruptcy of Lehman Brothers without government bailout was followed by a wave of conversions from shadow banks to commercial banks (including Goldman Sachs and Morgan Stanley). This paper provides a model framework to analyze the efficiency and stability of the banking sector following endogenous conversions between commercial banks and shadow banks caused by exogenous changes in the government guarantee policy. Securitization, which allows commercial banks to transfer a fraction of their balance sheet risks to shadow banks, is the key connection between these two banking sectors. The equilibrium securitization volume is determined by 1) commercial bankers’ trade-off between balance sheet risks and private benefit from deposit insurance, 2) shadow bankers’ ability to diversify their assets pool for sustaining higher leverage, and 3) the return on equity (ROE) between the two sectors. In a numerical experiment with a large drop in government guarantee to shadow banks, commercial banks expand, shadow banks shrink, and the banking sector is more stable under rational expectations. However, ROE in the whole banking sector is likely to decline and the exposure to the neglected tail risks increases as the shrinking shadow banking sector increases assets diversification to meet higher securitization requests from the expanding commercial banking sector.

Sources of Credit (with Dulani Seneviratne, Jerome Vandenbussche, and Peichu Xie)

We study if the heterogeneity in bank fundamentals contains information about future credit-related macrofinancial stability risks. We present our analyses based on (i) country-level measure of "riskiness of bank credit originations" and (ii) bank- and syndicated loan-level evidence of bank risk-taking patterns.